How Student Loans Affect Your Credit Score: The Full Picture

In the first quarter of 2025, 2.2 million Americans watched their credit scores drop by more than 100 points. Not because they took on new debt or stopped paying bills across the board. The student loan on-ramp period ended, previously invisible delinquencies appeared on credit reports, and the damage landed all at once. For 1 million of those borrowers, the drop was at least 150 points — enough to move someone from solid-credit territory into subprime in a single quarter.

That's the sharp edge of how student loans connect to your credit. The mechanics aren't mysterious, but they have consequences that follow you for seven years. Here's how all of it actually works.

What's Inside Your Credit Score (And Where Student Loans Touch It)

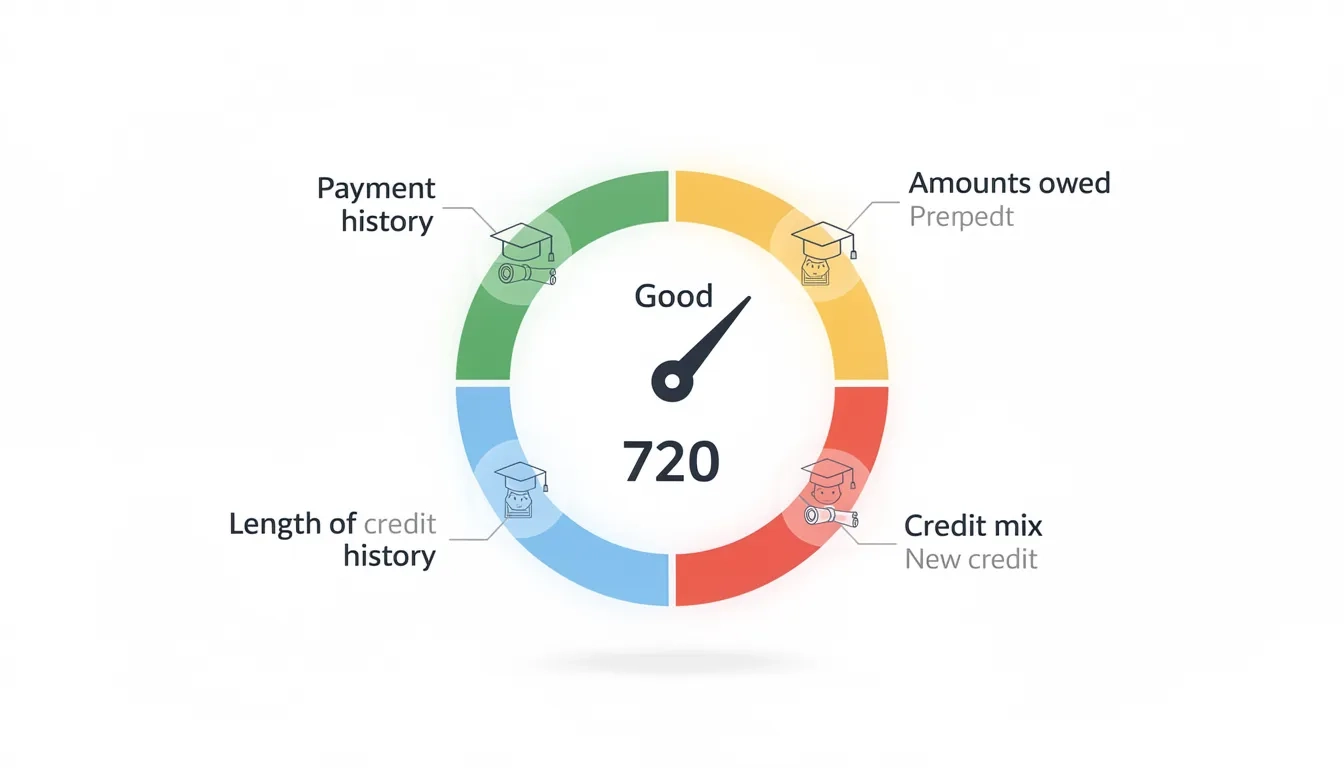

FICO scores — used in roughly 90% of lending decisions — break down across five weighted factors. Student loans can affect every single one. That's what makes them unusual compared to most financial products.

| Factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | On-time vs. late payments |

| Amounts owed | 30% | Total debt and utilization |

| Length of credit history | 15% | Age of oldest/newest accounts |

| Credit mix | 10% | Variety of debt types |

| New credit | 10% | Recent applications and new accounts |

When you first take out a student loan, you'll see a small, temporary dip from the hard inquiry and the drop in average account age. It usually reverses within six months. What happens after that depends entirely on how you manage the loan.

The Case for Student Loans Actually Helping Your Credit

Most people treat student loans as a pure liability. That's the wrong frame.

Credit mix diversification happens automatically with a student loan. You now hold installment debt alongside whatever revolving credit (credit cards) you have. FICO's credit mix factor rewards this because lenders want evidence you can handle different debt structures, not just credit cards.

Payment history accumulation is the real prize. Every on-time monthly payment is a positive data point hitting the 35% payment history factor. A borrower who strings together 48 consecutive on-time payments has a meaningfully stronger credit profile than someone who never borrowed anything. That's not obvious, but it's how the math works.

Account age also matters more than most people realize. Keeping a student loan open and in good standing over years grows the length of your credit history. Paying it off early closes the account — which can actually shorten your average account age and temporarily lower your score.

The counterintuitive truth: a student loan you're slowly paying down on time often does more for your credit score than one you paid off last year.

The Danger Zone: What Missing Payments Actually Does

This is where things get ugly fast. Not gradually. Fast.

A single missed payment can drop your score 60 to 110 points depending on your starting point. That's not a slow fade — it's a cliff. Borrowers with higher scores tend to fall further because they have more room to drop.

The New York Fed's Liberty Street Economics blog put precise numbers on this using Equifax data. For borrowers starting above 760 (the "superprime" tier), a 90-plus-day student loan delinquency caused an average score decline of 171 points. Borrowers in the 720–759 range saw 165-point drops. Near-prime borrowers (660–719) also lost 165 points on average. Even non-prime borrowers in the 620–659 range lost 143 points.

Think about what 171 points means in practice. A borrower at 780 slides to roughly 609 — from the top lending tier to subprime. Mortgage rates, car loan terms, credit card offers: all of it changes based on that number.

Late payments sit on your credit report for seven years. One rough stretch can affect your ability to buy a house a decade later. Putting that genie back in the bottle is a long, slow project.

Default: The Outcome to Avoid at Almost Any Cost

Federal student loan default kicks in after 270 days of non-payment. When it does, the consequences compound quickly:

- The full remaining balance may become immediately due

- Wages and tax refunds can be garnished without a court order

- Any cosigner on the loan takes the same credit hit

- You lose eligibility for additional federal financial aid

- The default notation stays on your report for seven years, even after you rehabilitate the loan

The 2025 situation made this scale concrete. According to the NY Fed's Consumer Credit Panel, over $250 billion in delinquent student debt appeared on credit reports when the on-ramp period expired. The "shadow delinquency rate" (loans 30-plus days past due that hadn't yet been reported) reached 15.6% by late 2024 — above the pre-pandemic peak of 14.8% in 2018.

Grace Zwemmer of Oxford Economics described the downstream chain: reduced credit limits, higher rates on new loans, lower borrowing capacity across the board. The credit hit doesn't stay in one lane.

Frankly, the scale of damage was preventable. Most of those 9.7 million affected borrowers had options — income-driven repayment, deferment, administrative forbearance. The information was technically available. But the system places the burden entirely on borrowers to find and request it.

Deferment and Forbearance: The Credit-Safe Pause

Here's a scenario that trips people up. You're struggling. You stop making payments, figuring you'll sort it out. Meanwhile, 30 days pass. Then 60. Then you call your servicer and ask about deferment.

That's exactly backwards.

Officially approved deferment does not hurt your credit score. When a servicer grants deferment, the loan reports to credit bureaus as "deferred" or "current" — not delinquent. Your payment history stays clean. Same goes for forbearance when properly granted.

But "officially approved" is the critical part. If you stop paying while waiting for your deferment application to process, those missed payments can still hit your report as late. The gap between "I applied" and "it was approved" is where borrowers get hurt.

| Payment Status | Credit Impact | Interest Still Accrues? |

|---|---|---|

| On-time monthly payments | Positive | Normal amount only |

| Officially approved deferment | Neutral | Depends on loan type |

| Officially approved forbearance | Neutral | Usually yes |

| Missed payments (no approval) | Negative | Yes, plus potential fees |

| Default (270+ days) | Severely negative | Yes, plus collection costs |

The financial difference between deferment and forbearance matters for your wallet even if both are credit-neutral. Interest typically keeps running during forbearance, growing your balance while you're not paying. Know which one you're in before you agree to it.

What the 2025 Data Tells Us

The pandemic pause created a kind of credit mirage. When student loans were marked current in 2020, previously delinquent borrowers saw median credit score improvements of 74 points — moving from 501 to 575. More than 4 million borrowers moved out of the below-620 bracket entirely during the pause.

Then the pause ended and reality reasserted itself.

The 2.4 million borrowers who became newly delinquent in early 2025 had previously held credit scores above 620. Good scores. And then, in a single quarter, many dropped below what mortgage lenders consider acceptable. Jason Ackerman of WealthRabbit framed it plainly: younger people are getting further behind on buying a house.

Credit score damage from student loans doesn't just sting in the moment. It delays the entire sequence of adult financial milestones — car loans, apartments, mortgages. Seven years is a long time to carry a mistake you could have avoided with a single phone call.

Practical Moves That Actually Protect Your Score

You don't have to be a passive participant in this system.

Set up autopay before your first payment is due. Federal loan servicers typically offer a 0.25% interest rate reduction for autopay enrollment (not life-changing, but it adds up). More importantly: you cannot accidentally miss a payment that happens automatically. This is the single highest-leverage habit available to you.

Call your servicer before you miss anything — not after. Income-driven repayment plans can reduce monthly payments to $0 for borrowers in low-income situations. Deferment is available for returning to school, job loss, economic hardship, and other qualifying events. The system has real flexibility built in; the catch is that you have to ask for it.

Monitor your credit reports regularly. You're entitled to free weekly reports from all three bureaus at AnnualCreditReport.com. Servicers do occasionally report incorrectly. Catching an error early means disputing it before it compounds.

If you're struggling to make payments, here's the decision framework:

- Temporary hardship (job loss, medical, returning to school): Apply for deferment or income-driven repayment immediately. Do not wait until after you've missed something.

- Long-term affordability problem: IDR plans cap payments at 5–10% of discretionary income. They exist for exactly this scenario.

- Payments are just tight: Call and ask about administrative forbearance. It often requires less paperwork than formal deferment.

- Already delinquent or in default: Ask about loan rehabilitation. Nine on-time payments over ten months can remove the default notation from your report, though late payment history prior to the default may remain.

One thing to reconsider: paying off your loans in a lump sum to close the account. If eliminating the debt makes financial sense for you, do it. But don't do it specifically to improve your credit score — closing the account can shorten your average credit history length and reduce your credit mix, which often produces a temporary score dip rather than a boost.

Bottom Line

Student loans sit at a strange intersection — they can build solid credit if managed well, or do serious damage if ignored. The 2025 data made the stakes impossible to miss.

- On-time payments build the most important credit factor (35%) month by month. No other habit comes close.

- Default and sustained delinquency can erase 143 to 171 points from your score depending on where you start, and that damage sticks for seven years.

- Deferment and forbearance work as credit protection — but only when officially approved. Never go silent with your servicer.

- The 2025 wave of credit damage affected 9.7 million borrowers in a single quarter, many of whom had options they didn't pursue.

- Enroll in autopay today. If you're struggling, call your servicer before the next payment date. That one conversation is worth more to your long-term financial health than most people appreciate.

Frequently Asked Questions

Do student loans hurt your credit score when you first take them out?

Yes, but mildly and temporarily. The initial hard inquiry from your loan application can trim a few points, and opening a new account lowers your average account age. Both effects typically fade within six months as you begin building positive payment history. The short-term dip is not a reason to avoid student loans.

Myth vs. reality: Does paying off student loans early improve your credit score?

This is one of the most widespread misconceptions. Paying off a loan closes the account, which can shorten your average credit history length and remove installment debt from your credit mix. Both changes can actually lower your score temporarily. For most borrowers, keeping the loan open with consistent on-time payments does more for long-term credit health than paying it off in one shot.

What happens to my credit score if I miss one student loan payment?

One payment that's 30 days late can drop your score by 60 to 110 points, with higher-score borrowers typically falling further. The late payment will remain on your credit report for seven years even after you catch up. This is why contacting your servicer before missing a payment — to request deferment, forbearance, or an IDR plan — matters far more than most people assume.

How long does student loan default stay on my credit report?

Seven years from the date of the first missed payment that led to the default. Federal loan rehabilitation (nine on-time payments over ten months) removes the default notation specifically, but late payment records that predated the default may still appear. Rehabilitation doesn't erase the history — it removes the "default" label, which is still meaningful for future lenders.

Does deferment show up negatively on my credit report?

No. When your servicer officially grants deferment, the loan reports as "deferred" to the credit bureaus — not delinquent. Your payment history factor stays intact. The cost is indirect: you're not accumulating positive payment history during the pause, and depending on your loan type, interest may continue growing your balance.

Can student loans help someone with no credit history build a score?

Yes, and this is genuinely underappreciated. For a borrower who has never had a credit card or loan, a student loan is often their first installment account. Making on-time payments builds both credit history length and payment history simultaneously. Many young borrowers who manage their loans well emerge from school with credit scores in the 680–720 range — a real head start.

Sources

- Credit Score Impacts from Past Due Student Loan Payments — NY Fed Liberty Street Economics

- Student Borrowers' Credit Scores Are Taking a Hit — CBS News

- Do Deferred Student Loans Affect Your Credit Score? — Rocket Money

- Do Student Loans Affect Your Credit Score? — HESC Loans

- Types of Credit and How They Affect Your FICO Score — myFICO