How College Endowment Tax Proposals Affect Students' Financial Aid and Tuition

When Congress passed the One Big Beautiful Bill and President Trump signed it into law on July 4, 2025, most of the headlines focused on spending cuts and tax brackets. Buried inside was a provision that could reshape what it costs to attend the country's most selective universities. The endowment tax on private colleges just jumped, and depending on where you go — or where you're hoping to go — the effects will land in your financial aid package, your tuition bill, or both.

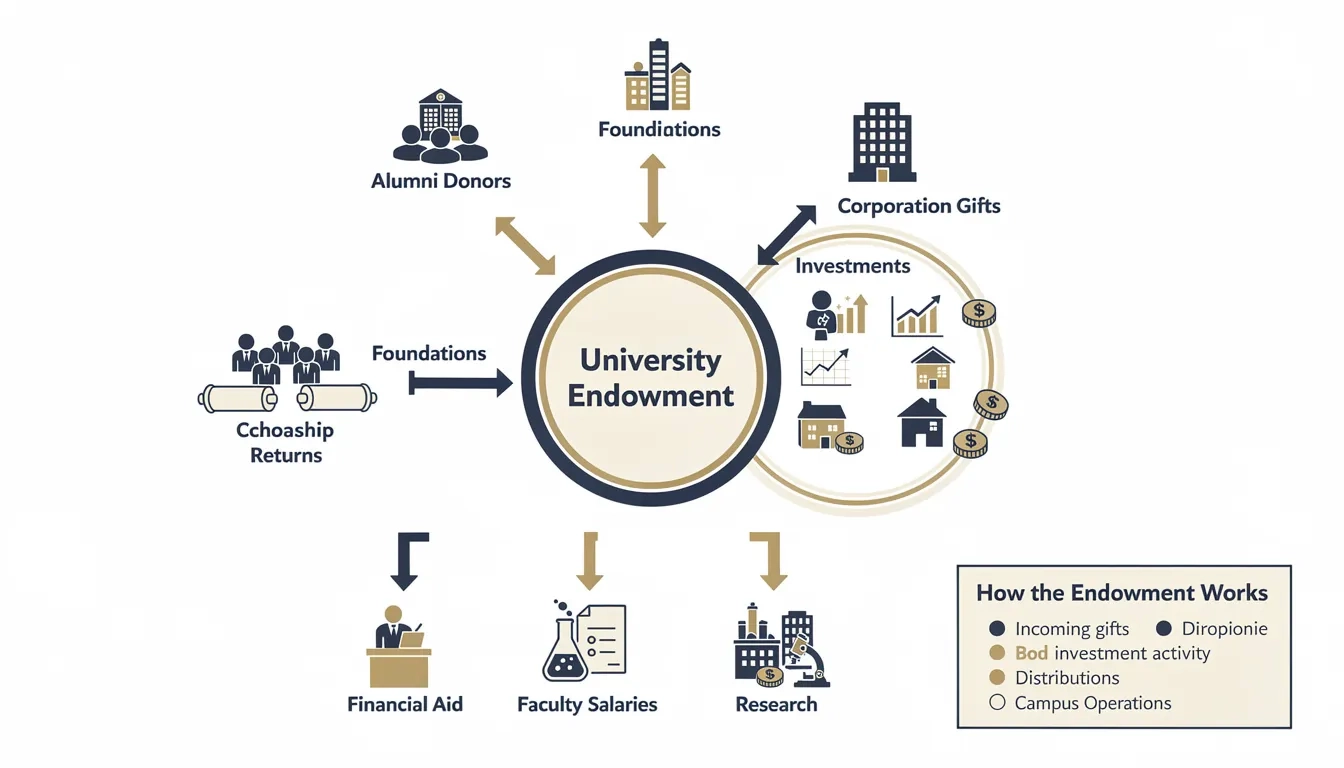

What an Endowment Actually Does

Most people picture a university endowment as a giant savings account collecting dust. It's more like a perpetual income machine. Donors give money, the university invests it, and each year the school spends a portion of the returns on operations. The principal stays intact — theoretically growing forever.

At Harvard, endowment distributions made up 37% of operating revenue in fiscal year 2024, generating roughly $2.5 billion in investment income. That money doesn't all go to marble buildings and faculty salaries. According to Steven Bloom, director of government relations at the American Council on Education, nearly half of endowment spending at these institutions goes directly to financial aid. "Almost 50 percent of endowment spending is on financial aid," Bloom said. "This money is going to come right out of that."

So when you tax endowment income more aggressively, you're not just hitting a balance sheet line. You're hitting scholarships.

A Quick History: The 1.4% Tax That Started It All

The federal government didn't always tax endowment income. That changed in 2017, when the Tax Cuts and Jobs Act introduced a 1.4% excise tax on net investment income for private universities with at least 500 tuition-paying students and endowments exceeding $500,000 per full-time student.

In 2023, only 56 universities actually paid it — collectively writing checks totaling about $380 million. That's a relatively small group: think Harvard, Yale, MIT, Stanford, Princeton, and roughly 50 others. Public universities like Michigan or UCLA were exempt entirely, regardless of endowment size.

The tax was controversial from the start. Critics called it a backdoor way to punish elite universities, which tend to lean left politically. Supporters argued that tax-exempt institutions sitting on billions while charging six-figure tuitions deserved closer scrutiny.

The 2025 Overhaul: A Tiered System With Real Bite

The One Big Beautiful Bill replaced the flat 1.4% rate with a three-tier structure based on how much endowment wealth a school has per enrolled student:

| Per-Student Endowment | New Tax Rate |

|---|---|

| $500,000 – $749,999 | 1.4% (unchanged) |

| $750,000 – $1,999,999 | 4% |

| $2,000,000 or more | 8% |

The top rate is effectively a 5.7x increase over the old flat rate. The provision takes effect for tax years after December 31, 2025, so schools are already doing the math on what they owe.

Only five universities currently sit in the 8% top bracket: Harvard, Yale, Princeton, Stanford, and MIT. Harvard's endowment works out to roughly $2.9 million per enrolled student, putting it firmly in the highest tier. Harvard President Alan Garber described a higher endowment tax as "the threat that keeps me up at night" — not a throwaway line from a university administrator, but a signal that this is being treated as a genuine financial crisis.

One notable wrinkle: the law now excludes international students from the enrollment count used to calculate per-student endowment. That change specifically drags Columbia University into a higher bracket than it would otherwise land in.

The Direct Hit to Financial Aid

Here's where students feel this most concretely. Elite universities use endowment income to fund "meets 100% of demonstrated financial need" programs — the policies that make Harvard free for families earning under $85,000 a year and heavily subsidized for families earning up to $200,000.

Those programs aren't funded by tuition. They're funded by endowment distributions. When the tax bill on that income goes up by hundreds of millions of dollars annually, the university faces a binary choice: find the money somewhere else, or cut the programs.

For Harvard, the additional tax burden from the new 8% rate could exceed $200 million per year. That's not theoretical. And the math gets uncomfortable fast when you consider that $200 million is a substantial portion of what Harvard spends on undergraduate financial aid.

Here's the decision tree most affected schools are working through:

- Draw down more from the endowment to cover both the tax and existing aid commitments — but this erodes long-term capital and violates the terms of many restricted gifts

- Cut financial aid by tightening eligibility thresholds or reducing grant amounts

- Raise tuition for students who pay full price, effectively cross-subsidizing the tax bill

- Reduce other expenses — research programs, staff, campus services

None of these options are painless, and most schools will probably do some combination of all four.

The Grad PLUS Twist: Students Already Paying Loans Take Another Hit

The endowment tax is only part of the story. The One Big Beautiful Bill also:

- Eliminates Grad PLUS loans, which currently allow graduate and professional students to borrow up to the full cost of attendance with no aggregate cap

- Caps Parent PLUS loans at $65,000 per student over the life of the loan

- Ties federal student aid eligibility to graduate earnings outcomes — meaning programs whose graduates don't earn enough post-graduation could lose access to federal loan dollars

Graduate students at law schools, medical schools, and MBA programs have depended on Grad PLUS loans to cover costs that institutional aid doesn't touch. Eliminating them doesn't make those programs cheaper. It just makes borrowing for them harder, likely pushing students toward private lenders at higher rates.

The Parent PLUS cap is similarly blunt. A family with two kids in college simultaneously now has a $130,000 combined borrowing limit, which at today's private university prices covers well under two full years of costs at many schools.

What Schools Outside the Top 5 Should Expect

The easy assumption is that only the Harvards of the world have anything to worry about. That's not quite right.

The 4% middle tier applies to schools with endowments between $750,000 and $2 million per student. Vanderbilt, Duke, Washington University in St. Louis, and Notre Dame all land in this range. For these schools, the tax increase isn't as dramatic as for the top five, but it's still a meaningful jump.

And because the per-student calculation now excludes international students, some institutions will find themselves pushed into a higher tier than expected. A school with a moderate endowment but a large international student body could see its effective per-student figure spike simply because fewer students are counted in the denominator.

Schools near the $750,000 threshold face particular uncertainty: a good investment year could push them into a higher bracket mid-decade, creating planning headaches that didn't exist under the old flat-rate system.

The Policy Debate: Do These Schools Deserve a Tax Break?

The honest answer is that this debate has two legitimate sides, and neither is as clean as its proponents claim.

The pro-tax argument goes like this: Harvard has a $50-billion-plus endowment, charges families $90,000 a year in sticker price, and pays no federal income tax on its investment gains. Meanwhile, a plumber making $80,000 a year is taxed on every dollar of income. Something about that arrangement bothers people — and it should.

The anti-tax argument is that endowment income isn't corporate profit. It's restricted charitable capital, legally obligated to serve educational purposes. Tax it heavily enough and you're not redistributing wealth — you're just making tuition more expensive for the middle-class students who most need need-based aid.

My read: the critics of elite universities have a point about accountability and transparency, but a blunt tax on investment income is a clumsy tool. The schools most likely to pass the cost on to students are the ones with the richest endowments and the most political capital to absorb the PR hit. The schools most likely to quietly cut aid without headlines are the ones in the middle tier that nobody is paying attention to.

According to TIFF (the Teacher's Insurance and Annuity Association Fund's research arm), raising the endowment tax from 1.4% to 21% over ten years would generate roughly $69.8 billion in federal revenue. The actual 8% top rate will raise considerably less — but even a fraction of that figure represents real money coming out of university budgets that would otherwise fund operations, research, and yes, scholarships.

Bottom Line

If you're a prospective student at a wealthy private university, here's what to actually do:

- Compare financial aid packages before committing. Schools affected by the new tax may quietly tighten their need-based formulas over the next two to three years. Get your aid offer in writing and ask admissions offices directly whether their "meets full need" policy is under review.

- Factor in graduate school debt separately. The elimination of Grad PLUS loans is a separate hit from the endowment tax, and it will affect graduate students before undergraduates feel the endowment crunch. If graduate or professional school is in your plan, model your borrowing under the new caps now.

- Don't assume public universities are immune. They're exempt from the endowment tax, but they compete for students with private schools. If elite privates become more expensive, expect selective publics to see more applicants — and become harder to get into.

The single most important thing to understand: endowment taxes don't disappear. They get passed on. The question is just who bears them, and how transparently the institution admits it.

Frequently Asked Questions

Does the endowment tax affect public universities like Michigan or UCLA?

No. The excise tax on endowment income applies only to private, nonprofit universities. Public institutions, regardless of endowment size, are fully exempt. That exemption doesn't mean public schools are unaffected by the broader bill — the Grad PLUS loan elimination and Parent PLUS caps hit students at all school types — but the endowment tax itself is a private-school issue.

Myth vs. reality: Do elite universities already pay plenty in taxes, making this a double tax?

This comes up a lot, and the framing is misleading. Private nonprofit universities are generally tax-exempt, meaning their endowment investment gains accumulate without federal income tax. The 1.4% excise tax introduced in 2017 was specifically designed to create some federal tax obligation on that investment income. Calling the new higher rate a "double tax" treats the prior exemption as a right rather than a policy choice — it isn't. That said, the jump from 1.4% to 8% is steep enough to genuinely affect institutional budgets.

How will I know if my financial aid package at an affected school will change?

The new tax takes effect after December 31, 2025, so schools are still calculating the impact. Watch for changes to institutional aid policies in 2026 and 2027 admissions cycles. If a school's "meets full need" language quietly disappears or its average grant size drops, that's the tax showing up. The National Association of Student Financial Aid Administrators (NASFAA) tracks institutional aid policy changes and is a good watchdog resource.

What should graduate students do now that Grad PLUS loans are being eliminated?

Start comparing private lender rates immediately. The federal Grad PLUS rate for 2024-25 was 9.08% — not cheap, but it came with income-driven repayment options and potential loan forgiveness. Private loans may or may not beat that rate depending on your credit, but they won't come with federal protections. If you're heading to law school, an MBA program, or medical school in the next few years, factor in the $65,000 Parent PLUS cap when modeling how you'll cover costs beyond what private borrowing covers.

Why does it matter that international students are excluded from the student count?

It moves schools into higher tax brackets. The per-student endowment figure is calculated by dividing total endowment assets by the number of "eligible" students — and the new law excludes international students from that count. A school with 20% international enrollment suddenly has a much smaller denominator, which inflates the per-student figure and can push the institution from a lower tax tier into a higher one. Columbia University is the school most explicitly called out in legislative discussions as being affected by this change.

Sources

- Trump Signs Spending Package Into Law, Imposing 8% Tax on Harvard's Endowment Income – The Harvard Crimson

- Endowment Taxes Could Climb to 21 Percent Under New Bill – Inside Higher Ed

- One Big Beautiful Bill Act Provision Would Modify Endowment Tax – McGuireWoods

- The Impact of Proposed Endowment Tax Changes – TIFF

- House Panel Advances Bill to Raise College Endowment Tax Up to 21% – Higher Ed Dive